Will Russia Sanctions Accelerate Inflation, Devalue US Dollar and Strengthen Chinese Yuan?

Russia is a commodities superpower. The nation's Eurasian landmass is rich in all kinds of natural resources from food to fuel to metals. To punish Moscow for invading Ukraine, the US and G-7 nations have imposed sanctions on Russia. These sanctions have effectively removed Russian commodities from the global supply chain, triggering double digit price increases for food, fuels and metals. Will the G-7 actions leave the US dollar much weaker? Will the Chinese currency, backed by commodities, gain strength at the expense of the US dollar and Euro? Will the era of commodity-backed money return? In a note to clients, Credit Suisse investment strategist Zoltan Pozsar has answered some of these questions. He says "this (Russia) crisis is not anything we have seen since President Nixon took the U.S. dollar off gold in 1971". "After this war is over, "money" will never be the same again.....and bitcoin (if it still exists then) will probably benefit from all this,” he adds.

|

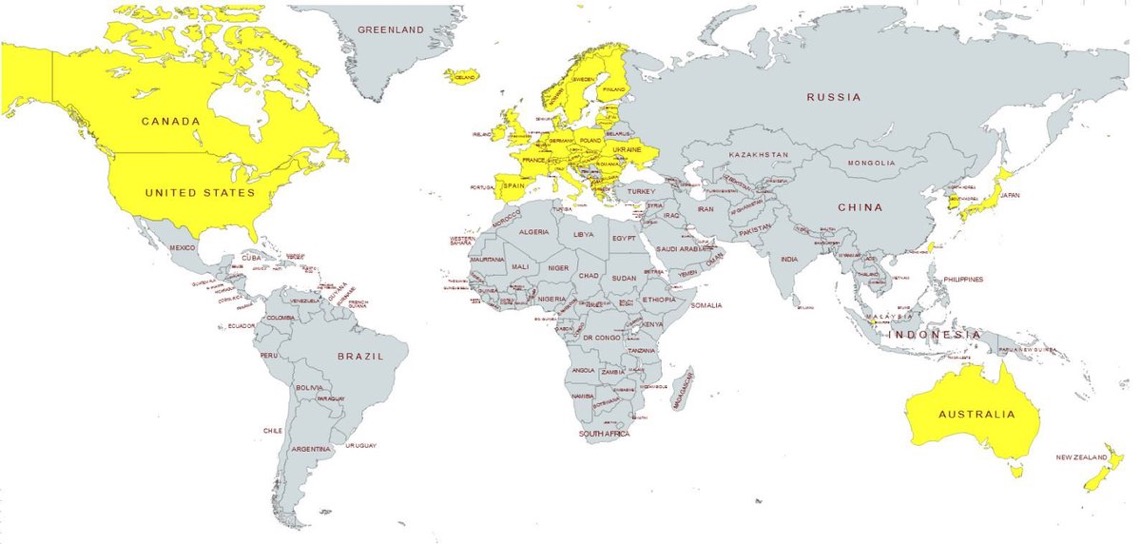

| Map of "International Community" Sanctioning Russia |

Post World War II History:

The current global financial system was created in Bretton Woods located in the US State of New Hampshire. Over 700 delegates representing 44 countries met in Bretton Woods in July 1944. The Bretton Woods System, now referred to as Bretton Woods I, required a currency peg to the U.S. dollar which was in turn pegged to the price of gold. This system collapsed in the 1970s but created a lasting influence on international currency exchange and trade through its development of the IMF and World Bank. Zoltan Pozsar believes it is now time for Bretton Woods III. What is Bretton Woods III? Here's how Zoltan Pozsar explains it:

"From the Bretton Woods era backed by gold bullion, to Bretton Woods II backed by inside money (Treasuries with un-hedgeable confiscation risks), to Bretton Woods III backed by outside money (gold bullion and other commodities)".

|

| Russia's Commodity Exports. Source: Bloomberg |

Commodity Superpower:

Russia is a vast country. Russian landmass extends from Europe to East Asia. It is one of the largest suppliers of oil, gas, metals and wheat. Russia is also a major exporter of fertilizer. China will likely take advantage of the western sanctions to buy up Russian commodities at lower prices.

Pozsar argues that while Western central banks cannot close the gap between Russian and non-Russian commodity prices as sanctions lead them in opposite directions, the People’s Bank of China can “as it banks for a sovereign who can dance to its own tune.”

“If you believe that the West can craft sanctions that maximize pain for Russia while minimizing financial stability risks and price stability risks in the West, you could also believe in unicorns,” Pozsar wrote.

|

| Pre-Ukraine War Inflation in US. Source: Wall Street Journal |

Bretton Woods III:

Pozsar argues that the Bretton Woods II collapsed when the G7 countries seized Russia’s foreign exchange (FX) reserves, leading to a rise of outside money – reserves kept as commodities – over inside money – reserves kept as liabilities of global financial institutions.

|

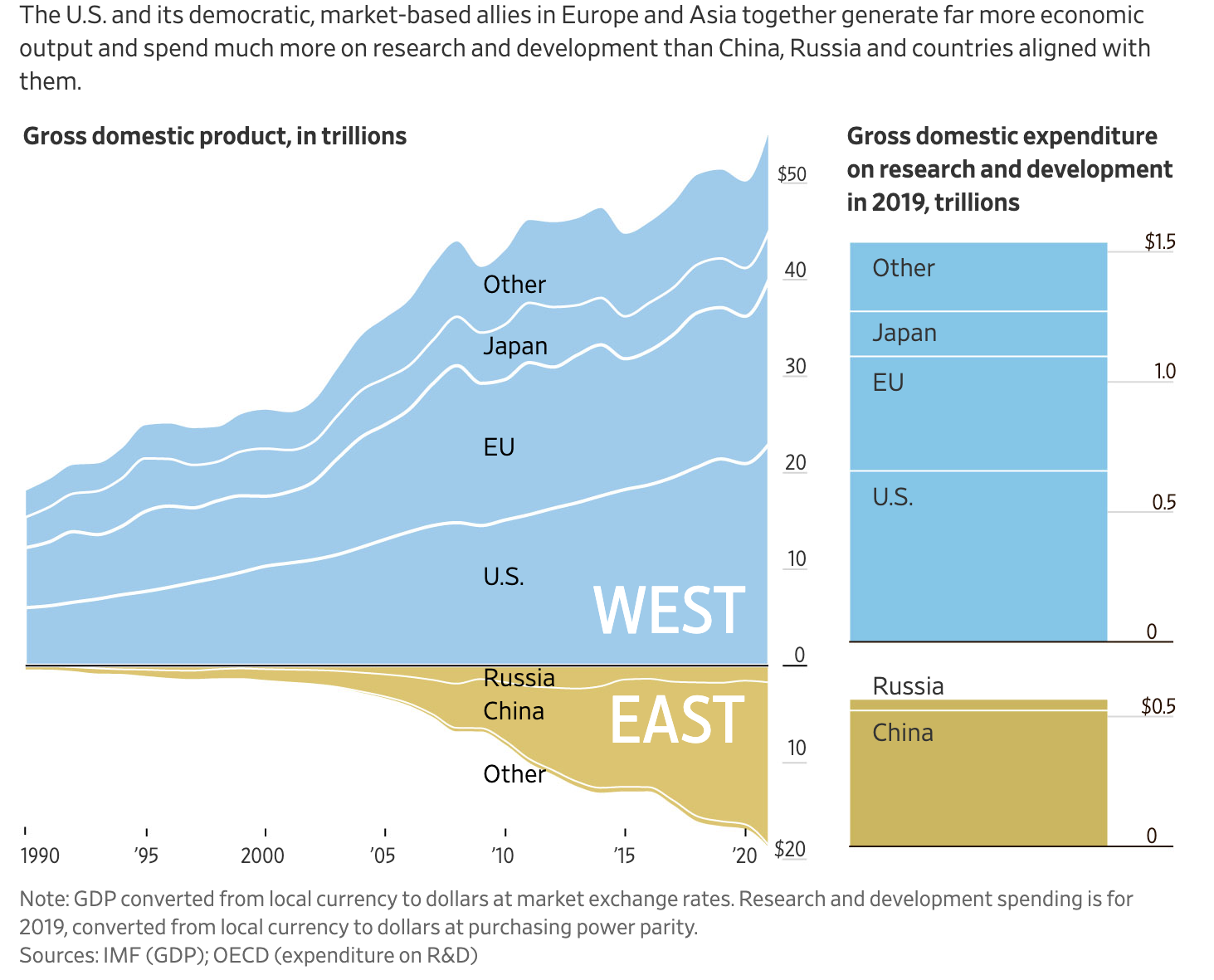

| East vs West Economic Output. Source: Wall Street Journal |

"We are witnessing the birth of Bretton Woods III – a new world (monetary) order centered around commodity-based currencies in the East (Chinese Yuan) that will likely weaken the Eurodollar system and also contribute to inflationary forces in the West,” Zoltan wrote.

Related Links:

Pakistani-American Banker Heads SWIFT, the World's Largest Interbank Payment System

Pakistani-Ukrainian Billionaire Zahoor Sees "Ukraine as Russia's Afghanistan"

Ukraine Resists Russia Alone: A Tale of West's Broken Promises

Ukraine's Lesson For Pakistan: Never Give Up Nuclear Weapons

Can the Chinese Yuan Replace the US Dollar?

Ukraine's Muslim Billionaire Akhmetov Holds Balance of Power

Ukraine's Muslims Oppose Russia

Comments

Keeping Russian banks from using SWIFT is not the financial nuclear weapon some have suggested.

https://www.washingtonpost.com/politics/2022/03/07/swift-sanctions-russia-ukraine-banking/

While the United States might fear the growth of new messaging services in the future, this case isn’t likely to bring significant blowback. Russia is unlikely to use alternative financial channels, because the existing ones all have problems. For example, executing transactions over telephone or fax, or by using credit or debit cards that fuse communications technologies with transactions. That’s outdated and will not scale to the degree Russia would need.

Alternative financial communication networks are either in their infancy or depend on the SWIFT network. The Bank of Russia created a financial messaging system (FMS) after the 2014 Ukraine crisis — but it includes only 400 users and therefore isn’t that useful. China’s Cross-Border Interbank Payment System (CIPS) has about three times FMS’s users — but SWIFT includes nearly 10 times as many users as CIPS. What’s more, CIPS isn’t an alternative to SWIFT; it depends on SWIFT for international messaging.

Russian banks not facing sanctions may turn to CIPS. But China may be reluctant to welcome sanctioned banks, lest it jeopardize its use of SWIFT.

---------------

Two days after Russia launched an attack on Ukraine, the United States, Canada and European allies agreed to disconnect a handful of Russian banks from SWIFT, the Society for Worldwide Interbank Financial Telecommunication. These “de-SWIFTed” Russian banks would no longer be able to use the financial interface to transfer money.

The long-standing, and controversial, threat to disconnect Russia from the SWIFT network has been touted as a centerpiece of the West’s retaliation. How big is it, really? And how will it affect the United States and its use of financial power in the future?

The limits of de-SWIFTing

SWIFT connects more than 10,000 financial institutions in a communications network where orders are sent and received. This messaging service enables participating banks to settle commercial, financial and foreign-exchange payments. Cutting banks off from SWIFT means they can no longer use the network to exchange information.

But keeping banks from accessing SWIFT is not, on its own, the financial nuclear weapon some suggest. Denying access to SWIFT, for example, does not stop banks from communicating or transacting with the 11,000 financial institutions outside the SWIFT network. Disconnected banks that do not face sanctions are free to use alternative messaging networks to settle payments.

In fact, without sanctions on actual money transfers, denying countries access to SWIFT could undermine the messaging service by encouraging users to rely on other financial communication networks.

Today, SWIFT continues to be dominated by major U.S. financial institutions, with 40 percent of recorded transactions occurring in U.S. dollars. Making the U.S.-centered financial order less attractive is precisely the type of collateral damage the United States seeks to avoid.

https://www.wsj.com/articles/saudi-arabia-considers-accepting-yuan-instead-of-dollars-for-chinese-oil-sales-11647351541

China introduced yuan-priced oil contracts in 2018 as part of its efforts to make its currency tradable across the world, but they haven’t made a dent in the dollar’s dominance of the oil market. For China, using dollars has become a hazard highlighted by U.S. sanctions on Iran over its nuclear program and on Russia in response to the Ukraine invasion.

China has stepped up its courtship of the Saudi kingdom. In recent years, China has helped Saudi Arabia build its own ballistic missiles, consulted on a nuclear program and begun investing in Crown Prince Mohammed bin Salman’s pet projects, such as Neom, a futuristic new city.

----------

The talks with China over yuan-priced oil contracts have been off and on for six years but have accelerated this year as the Saudis have grown increasingly unhappy with decades-old U.S. security commitments to defend the kingdom, the people said.

The Saudis are angry over the U.S.’s lack of support for their intervention in the Yemen civil war, and over the Biden administration’s attempt to strike a deal with Iran over its nuclear program. Saudi officials have said they were shocked by the precipitous U.S. withdrawal from Afghanistan last year.

China buys more than 25% of the oil that Saudi Arabia exports. If priced in yuan, those sales would boost the standing of China’s currency.

It would be a profound shift for Saudi Arabia to price even some of its roughly 6.2 million barrels of day of crude exports in anything other than dollars. The majority of global oil sales—around 80%—are done in dollars, and the Saudis have traded oil exclusively in dollars since 1974, in a deal with the Nixon administration that included security guarantees for the kingdom.

---------

Meanwhile the Saudi relationship with the U.S. has deteriorated under President Biden, who said in the 2020 campaign that the kingdom should be a “pariah” for the killing of Saudi journalist Jamal Khashoggi in 2018. Prince Mohammed, who U.S. intelligence authorities say ordered Mr. Khashoggi’s killing, refused to sit in on a call between Mr. Biden and the Saudi ruler, King Salman, last month.

It also comes as the U.S. economic relationship with the Saudis is diminishing. The U.S. is now among the top oil producers in the world. It once imported 2 million barrels of Saudi crude a day in the early 1990s but those numbers have fallen to less than 500,000 barrels a day in December 2021, according to the U.S. Energy Information Administration.

By contrast, China’s oil imports have swelled over the last three decades, in line with its expanding economy. Saudi Arabia was China’s top crude supplier in 2021, selling at 1.76 million barrels a day, followed by Russia at 1.6 million barrels a day, according to data from China’s General Administration of Customs.

https://www.ft.com/content/9294890a-593c-442b-bc53-13099d14d36f

Islamabad strains ties with the west after refusing to condemn Moscow’s invasion of Ukraine

https://www.ft.com/content/9294890a-593c-442b-bc53-13099d14d36f

Khan visited Moscow on the same day Russia invaded Ukraine last month, the first visit by a Pakistani premier in more than 20 years. The EU, UK, Australia and others “urged” Pakistan to condemn Russia in a UN General Assembly vote. Pakistan abstained from the vote, with Khan attacking the western countries at a campaign rally for treating Pakistanis like “slaves”. Tarin said he hoped Russian officials would soon visit the country to finalise the deal for the Pakistan Stream pipeline following Khan’s Moscow visit. The pipeline, to be built by a collection of Russian companies, is estimated to cost more than $2bn. Recommended News in-depthOil & Gas industry The Soviet pipeline that keeps Europe hooked on Moscow’s oil Well before the latest surge in oil and gas prices, Pakistan was struggling with a widening current account deficit and double-digit inflation exacerbated by rising global commodity prices. Pakistan last month resumed a contentious $6bn IMF programme to stabilise the country’s balance of payments and shore up government revenues. But Tarin said the conflict presented a new “crisis” that would push up the cost of imports including energy and wheat, which Pakistan previously sourced from both Russia and Ukraine. Higher prices following the US’s ban on Russian oil and gas imports would affect Pakistan “very negatively” unless Washington unlocked alternate energy sources, he said. Energy makes up about a quarter of Pakistan’s import bill. He added that a nuclear deal between the US and Iran would allow Islamabad to revive a plan to build a pipeline delivering gas directly from Iran to neighbouring Pakistan, which is suspended because of international sanctions. “If there’s a deal . . . this is the cheapest [option]. It’s next door,” he said. “It’ll be very good for us.” Tarin said it was “only fair that people should respect” Pakistan’s “neutral” stance. The west “have been our allies for a very long time. We’re listening to them, but we told them, ‘Listen, we don’t believe in taking sides. We’re with you as much as China and others’,” he added.

In an economic Cold War pitting China and Russia against the U.S. and its allies, one side holds most of the advantages. It just has to use them.

https://www.wsj.com/articles/how-the-west-can-win-a-global-power-struggle-11647615557?mod=Searchresults_pos1&page=1

In the years preceding its invasion of Ukraine, Russia set out to sanction-proof its economy by developing local substitutes for key foreign products, such as microprocessors. The only problem: Since it lacks advanced semiconductor fabrication capacity, production of these Russian-designed chips was outsourced, mainly to Taiwan Semiconductor Manufacturing Co. After the invasion of Ukraine, Taiwan joined the U.S. in banning the export of sensitive technology to Russia. TSMC immediately promised to comply.

Russia may be an energy superpower but Taiwan is a semiconductor superpower, and semiconductors are harder to replace than oil. Therein lies a critical insight about the emerging Cold War between Russia and China on one side and the West—the U.S. and its democratic allies—on the other. This Cold War will be much more of an economic contest than the first, and the balance of economic power favors the U.S. and its allies. And it’s not even close.

Chinese President Xi Jinping likes to boast, “The East is rising, the West is declining.” When the rivalry was limited to China and the U.S., this had some resonance: At current rates of growth, China will surpass the U.S. as the world’s largest economy as soon as 2030 despite U.S. gains in the last year.

But with China partnered with Russia and the West more united than ever, this is turning into a contest of alliances, and Xi couldn’t be more wrong. In this framing, “East” and “West” are not geographic, but geopolitical, labels. If “the East” is defined as those countries with which China is closely aligned (it eschews formal alliances), only China is any sense rising. Russia was a stagnating petrostate even before sanctions eviscerated its economy. The others, such as Kazakhstan, Belarus, Pakistan, North Korea, Cambodia and Laos, are poor, slow-growing, or both. The West, defined as the European Union, the anglosphere (the U.S., Australia, Canada, Britain and New Zealand) and East Asia’s three big, rich democracies, Japan, South Korea and Taiwan, may not be growing rapidly, but it is growing and has a gigantic head start. As former U.S. Treasury Secretary Henry Paulson said a Chinese official once told him: “You have all the good allies.”

By itself, China accounted for 18% of global gross domestic product at current exchange rates last year, based on International Monetary Fund data. Adding Russia and their assorted allies brings the total to just 20%. The U.S., meanwhile, accounted for 24%, and adding its allies vaults the total to 59%.

While sanctions on Russia demonstrate the West’s control of the global financial system, long-run economic advantage will come from technology and knowledge. In pure science—such as space travel and atomic energy—Russia and China certainly hold their own. But in commercially useful technology, Western companies lead in almost every field, from commercial aviation and biotechnology to semiconductors and software.

“If you have a coherent strategy across the major democracies, you’re in an enormously robust position in terms of financial, economic and technological leverage,” said former Australian Prime Minister Kevin Rudd, now president of the Asia Society think tank.

In an economic Cold War pitting China and Russia against the U.S. and its allies, one side holds most of the advantages. It just has to use them.

https://www.wsj.com/articles/how-the-west-can-win-a-global-power-struggle-11647615557?mod=Searchresults_pos1&page=1

Of course the East plays a central role in the global economy. As recent market turmoil illustrates, Russia is a key supplier of not just oil and gas but metals such as palladium, used in catalytic converters, and nickel. China dominates manufacturing of countless goods whose value became abundantly clear during the pandemic, when demand for some, such as protective personal equipment, skyrocketed.

To a great extent these strengths reflect Russia’s comparative advantage in geology and China’s in factory labor. The West’s comparative advantage is in knowledge. That’s why Russia and China court Western investment. For example, to develop a complex liquefied natural gas (LNG) project in the Arctic, Russia relied on Norwegian, French and Italian contractors for essential expertise, research firm Rystad Energy notes.

Catching up with the West is no easy task, as semiconductors illustrate. Western companies dominate all the key steps in this critical and highly complex industry, from chip design (led by U.S.-based Nvidia, Intel, Qualcomm and AMD and Britain’s ARM) to the fabrication of advanced chips (led by Intel, Taiwan’s TSMC and South Korea’s Samsung ) and the sophisticated machines that etch chip designs onto wafers (produced by Applied Materials and Lam Research in the U.S., the Netherlands’ ASML Holding and Japan’s Tokyo Electron ).

Russia and China have made efforts to reduce this dependence. Russia developed locally designed microprocessors called Elbrus and Baikal to run data centers, cybersecurity operations and other applications. Though neither has achieved significant market share, they “represent the pinnacle of local design capability,” said Kostas Tigkos, principal at Jane’s, a defense intelligence provider. Russia hoped that they would eventually displace chips made by Intel and AMD, he said. “This would not only have been the foundation for diversifying their installed base, but a stepping stone for exports of those processors to other friendly nations.” But without manufacturers like TSMC to make the chips, Russia is facing “the complete disintegration of their aspirations to develop their own industry.”

China has a much bigger semiconductor industry than Russia, and its partly state-owned national champion, Semiconductor Manufacturing International Co. (SMIC), could in theory make Russia’s chips, but that would take at least a year, Mr. Tigkos said. Moreover, its efforts to catch up to its Taiwanese competitor have been set back by sanctions. In 2020 the U.S. required companies using American technology to obtain a license to sell to SMIC. This effectively limited its ability to acquire advanced equipment from Netherlands’ ASML, which is critical for “any country that wants to have a competitive semiconductor industry,” Mr. Tigkos said.

Why does all this matter to the outcome of the geopolitical contest? Over time economic weight, strength and vitality are what allow countries to sustain military capability, achieve and maintain technological superiority, and remain attractive partners for other countries.

In an economic Cold War pitting China and Russia against the U.S. and its allies, one side holds most of the advantages. It just has to use them.

https://www.wsj.com/articles/how-the-west-can-win-a-global-power-struggle-11647615557?mod=Searchresults_pos1&page=1

Yet GDP does not automatically equate to strategic influence. To win a Cold War, it’s not enough for the West to hold the best economic cards, it has to know how to play them. Economic statecraft, as this is called, does not come naturally to the West: Its institutions are built on the assumption that companies are private enterprises, not instruments of the state. They do business wherever it’s profitable, regardless of their home countries’ strategic interests.

No such division exists in Russia and China. Russian President Vladimir Putin used state control of key industries such as natural gas to reward or threaten neighbors. The Chinese Communist Party insists that state-owned and even private enterprises give priority to the state’s interests. In return, China tilts the playing field in those companies’ favor at home and abroad. Chinese state-sponsored hackers steal commercial secrets from Western companies, the U.S. has alleged. China is a master of economic coercion, punishing countries such as Australia or Lithuania or companies that cross its diplomatic red lines by depriving them of access to the Chinese market, knowing other countries and companies will eagerly take their place.

China has also learned how to play companies and countries in the West off against one another—favoring whoever promises to share more of its technology with Chinese partners, or avoids criticism of China.

Western governments, such as Germany, exaggerate China’s economic power and underappreciate their own, said Luke Patey, an expert on China’s international economic strategy at the Danish Institute for International Studies. “Germany has a full house when it comes to geoeconomics but plays like it has a pair of threes,” Mr. Patey said. The West frets that Chinese companies lead in fifth-generation telecommunications equipment—such as Huawei Technologies—and electric vehicle batteries. But, he said, “We sell short the fact that up there with Huawei are Ericsson, Nokia and Samsung,” based in Sweden, Finland and South Korea, respectively. Meanwhile Japan’s Panasonic and South Korea’s LG “are making the most sophisticated electric vehicle batteries in the world.”

For the West to play this game, it will have to more skillfully employ its ample economic assets toward geopolitical ends. The sanctions on Russia show that it can: The West showed a remarkable breadth and unity in its willingness to sustain significant economic discomfort in order to punish Russia. When the Trump administration imposed export controls on China, Taiwan did not join in but its companies were forced to comply because they use U.S. technology. This time Taiwan itself locked arms with the U.S. “Taiwan strongly condemns Russia’s invasion of Ukraine. Our country joins the U.S., EU & other like-minded partners in sanctioning Russia,” its Ministry of Foreign Affairs tweeted.

In an economic Cold War pitting China and Russia against the U.S. and its allies, one side holds most of the advantages. It just has to use them.

https://www.wsj.com/articles/how-the-west-can-win-a-global-power-struggle-11647615557?mod=Searchresults_pos1&page=1

The West makes up for the shortage of homegrown talent through immigration. A study by the Peking University Institute of International and Strategic Studies earlier this year lamented that 34% of China’s top artificial intelligence talents worked in China while 56% worked in the U.S., whose “relatively relaxed and innovative scientific research environment is…favored by scientific and technological talents.” Tech entrepreneurs are motivated by freedom and wealth, both of which are slipping out of reach in China and Russia.

Thus a key factor in whether the West can sustain its edge is whether it can remain a magnet for talent. Yet the West’s openness to trade and immigration and even its commitment to democracy have come under stress. In the last decade support in Europe and the U.S. has surged for right-wing populists opposed to immigration and free trade, skeptical of NATO, and admiring of Mr. Putin. These include Marine Le Pen, a contender for president in France’s elections this spring, and former U.S. President Donald Trump, who may seek the White House again in 2024. Democracy has backslid in Hungary, Poland and the U.S., according to the think tank Freedom House.

This points to the final and perhaps biggest challenge for Western nations. Having shown how effectively they can sever ties with Russia, can they be equally effective in strengthening ties with each other and unaligned players like India, Brazil and Vietnam—and thus be an attractive alternative to the autocratic East?

After World War II the U.S. used trade to strengthen other democracies and bind allies, and its reward was a democratic and prosperous West. Yet since the 2000s Americans have soured on this model, as expanded trade with the likes of China brought economic turmoil and little geopolitical benefit. Mr. Trump saw trade as a zero-sum game and hit allies and adversaries alike with tariffs. He pulled the U.S. out of the Trans-Pacific Partnership with 11 other Pacific rim countries, a pact covering not just tariffs but investment, intellectual property, data and the behavior of state-owned enterprises, intended as an alternative to China. Mr. Biden has resolved tariff disputes but pushed to expand “Buy American” regulations that penalize imports. He has offered no trade-agreement analog to his expanded military ties with allies in Europe and Asia, although he has promised a less ambitious “Indo-Pacific Economic Framework.”

In an economic Cold War pitting China and Russia against the U.S. and its allies, one side holds most of the advantages. It just has to use them.

https://www.wsj.com/articles/how-the-west-can-win-a-global-power-struggle-11647615557?mod=Searchresults_pos1&page=1

Meanwhile, China is fast cultivating its own economic sphere of influence, via foreign investment, its “Belt and Road” infrastructure initiative, and trade agreements, even applying to join the TPP, renamed the Comprehensive and Progressive Agreement for Trans-Pacific Partnership.

“China has studied very carefully the American postwar model of how their global and regional military domination was augmented by financial and economic domination,” said Mr. Rudd. China, he said, seeks to achieve its foreign policy aims by making countries throughout Asia, including American allies, dependent on its trade and investment, and eventually its currency. Mr. Rudd urged the U.S. to return to the TPP and revive a similar pact with Europe. The U.S. needs to recognize where its strategic advantage lies, “which is through free trade, open commerce and open capital flows.”

Fed chief says China has been working on currency matters

Powell says Ukraine war may serve as accelerant to China moves

Powell: Fed Needs to Be 'Nimble' Amid Ukraine Crisis

Federal Reserve Chair Jerome Powell said the Ukraine war could have the effect of accelerating China’s moves to develop alternatives to the current dollar-dominated international payments infrastructure.

Powell was questioned Thursday in a Senate Banking Committee hearing on how China might view the U.S.-led efforts to isolate Russia’s economy, especially by damaging its ability to use the dollar.

https://www.bloomberg.com/news/articles/2022-03-03/powell-says-war-may-speed-china-moves-to-insulate-against-dollar

Silicon Valley’s increasingly aggressive stance against Russia could fuel the growth of rivals there and in China, Iran, too

https://www.washingtonpost.com/technology/2022/03/03/us-russia-technology-dependence/

Withholding technology can be a soft-power weapon to potentially turn a population against its leaders. Yet it also can be costly to the U.S. economy, slow to deliver results and scattershot in its effects — much more likely to affect ordinary Russians using their iPhones than generals firing missiles into Ukrainian cities.

There is another cost, as well. The United States’ dominance of global technology, experts warn, was built over generations but could be eroded in just a few years as rival powers — and especially Russia and China — invest billions of dollars to develop alternative technologies at home, in part to decrease U.S. leverage at moments such as these.

Even as Russians furiously buy iPads, Android devices and Windows-based computers, President Vladimir Putin is pushing hard to wean the country from Western technologies. And if Russia and other U.S. rivals succeed, there also could be long-term damage to the ability of American intelligence agencies — particularly skilled in exploiting U.S.-made tech — to track developments in the next conflict, experts say.

The upshot is that although technology sanctions can be unquestionably powerful, it’s a power that, when deployed, can spark backlashes that undermine its long-term utility. Depriving rivals of American-made technology also threatens the future global prospects of an industry that has driven U.S. economic growth for most of this century. The rise of a Russian Google — or a Chinese Facebook or an Iranian YouTube — are not theoretical developments. They are happening already.

“When you cut them off from American tech, they will find alternatives,” said Peter Micek, general counsel for Access Now, a human rights group that lobbies to keep Internet services available to people worldwide.

U.S. officials and technology executives are attempting to navigate this chessboard of risk and reward as they assemble a potent set of punitive moves against Russia.

The result has been growing restrictions on hardware, with Apple joining others in blocking sales to Russia, and moves by major social media platforms to curb the spread of Russian propaganda through its state-funded RT information service — often in response to the demands of Western governments. Digital purchasing tools, such as Apple Pay, also have stopped working as Western sanctions cut off Russian banks for ordinary operations.

But calls by Ukrainian officials to deprive Russians in general of access to social media and even the Internet itself have sparked significant resistance from both the companies and digital rights groups, which argue that the likes of Twitter, WhatsApp and Telegram are key to delivering information in Russia. They often are the only sources of news on the horrors Putin is inflicting on Ukrainians at a time when his control over national news media is nearly total.

The Russian government, meanwhile, has been squeezing these same companies, throttling Facebook and Twitter, and threatening action against Google in retaliation for its YouTube subsidiary limiting access to RT in response to demands by Western governments.

But as this conflict plays out, the idea of depriving Russia of software updates or online support from U.S. companies has not gained traction, even though such moves could gradually erode the functioning of technological tools used every day by the Russian government and its citizens.

By M. K. BHADRAKUMAR

https://www.indianpunchline.com/bidens-reality-check-in-europe/

The unkindest cut of it all is that the Russian Defence Ministry chose Biden’s trip as the perfect backdrop to frame the true proportions of success of its special operation in Ukraine. The US and NATO’s credibility is perilously close to being irreparably damaged, as the Russian juggernaut rolls across Ukraine with the twin objectives of ‘demilitarisation’ and ‘denazification’ in its sights.

The Russian General Staff disclosed on Friday that the hyped up Ukrainian Armed Forces, trained by the NATO and the US, have sustained crippling losses: Ukrainian air force and air defence is almost completely destroyed, while the country’s Navy no longer exists and about 11.5% of the entire military personnel have been put out of action. (Ukraine doesn’t have organised reserves.)

According to the Russian General Staff’s deputy head Colonel General Sergey Rudskoy, Ukraine has lost much of its combat vehicles (tanks, armoured vehicles, etc.), one-third of its multiple launch rocket systems, and well over three-fourths of its missile air defence systems and Tochka-U tactical missile systems.

Sixteen main military airfields in Ukraine have been put out of action, 39 storage bases and arsenals destroyed (which contained up to 70% of all stocks of military equipment, materiel and fuel, and more than 1 million 54000 tons of ammunition.)

Interestingly, following the intense high-precision strikes on the bases and training camps, foreign mercenaries are leaving Ukraine. During the past week, 285 mercenaries escaped into Poland, Hungary and Romania. Russian forces are systematically destroying the Western shipment of weapons.

Most important, the mission to liberate Donbass is about to be accomplished. Simply put, the main objectives of the first phase of the operation have been achieved.

Apart from Kiev, Russian troops have blocked the northern and eastern cities of Chernigov, Sumy, Kharkov and Nikolaev, while in the south, Kherson and most of Zaporozhye region are under full control — the intention being to not only to shackle Ukrainian forces but to prevent their grouping in Donbass region. (See my article Dissecting Ukraine imbroglio, Tribune, March 21, 2022)

“We did not plan to storm these cities from the start, in order to prevent destruction and minimise losses among personnel and civilians,” Rudskoy said. But, he added, such an option is not ruled out either in the period ahead.

It stands to reason that Washington and European capitals are well aware that the Russian operation is proceeding as scheduled and there is no stopping it. Thus, the NATO’s extraordinary summit on March 24 confirmed that the alliance is unwilling to get into a military confrontation with the Russian Army.

Instead, the summit decided to strengthen the defence of its own territories! Four additional multinational NATO combat groups of 40,000 troops will be deployed in Bulgaria, Hungary, Romania and Slovakia on a permanent basis. Poland’s proposal to deploy NATO military units in Ukraine was outright rejected.

However, Poland has certain other plans, namely, to deploy contingents to the western regions of Ukraine to support the ‘fraternal Ukrainian people” with the unspoken agenda of reclaiming control over the historically disputed territories in the those regions. What Faustian deal has been struck in Warsaw on March 25 between Biden and his Polish counterpart Duda remains unclear. Clearly, vultures are circling Ukraine’s skies. (See my blog Biden wings his way to the borderlands of Ukraine, March 24, 2022)

https://www.bloomberg.com/news/articles/2022-03-28/pakistan-s-energy-crunch-spurs-barter-trade-for-afghani-coal

Cash-strapped Pakistan can’t afford to buy fuel on the spot market and is either skipping purchases or turning to alternatives such as Afghani coal as it grapples with a worsening energy crisis.

State-owned Pakistan LNG Ltd. didn’t award a recent purchase tender seeking several shipments of liquefied natural gas through May due to high offer prices. Cement manufacturers, meanwhile, are buying coal from Afghanistan at roughly half the price of shipments from regular supplier South Africa.

Russia's invasion of Ukraine on Feb. 24 sparked sweeping sanctions that ripped the country out of the global financial fabric and sent its economy reeling.

A month on, Russia's currency has lost a large part of its value and its bonds and stocks have been ejected from indexes. Its people are experiencing economic pain that is likely to last for years to come.

Below are five charts showing how the past month has changed Russia's economy and its global standing:

In 2020, Russia was the world's 11th-largest economy, according to the World Bank. But by the end of this year, it may rank no higher than No. 15, based on the end-February rouble exchange rate, according to Jim O'Neill, the former Goldman Sachs economist who coined the BRIC acronym to describe the four big emerging economies Brazil, Russia, India and China.

Recession looks inevitable. Economists polled by the central bank predicted an 8% contraction this year and for inflation to reach 20%.

Forecasts from economists outside Russia are even gloomier. The Institute of International Finance predicts a 15% contraction in 2022, followed by a 3% contraction in 2023.

"Altogether, our projections mean that current developments are set to wipe out the economic gains of roughly fifteen years," the IIF said in a note.

https://twitter.com/haqsmusings/status/1508946186815770624?s=20&t=0bTDjFwjnkYoDd53P9u_wA

Some of the accounts used fake profile pictures, raising researchers’ suspicions. Others racked up thousands of retweets on their pro-Putin posts, despite having few followers and low engagement on the rest of their tweets.

Although the activity suggested the accounts may be inauthentic, there was no hard evidence that they were part of a coordinated influence campaign aimed at shifting sentiment about the war in India. A Twitter spokeswoman said the company was still investigating.

The challenge of identifying influence campaigns is further complicated by the split of public opinion in India. While some people have vehemently opposed the war, others have vocally backed Russia and held marches to show support.

“Russia and India have longstanding and deep security and economic relations,” said Graham Brookie, director of the Atlantic Council’s digital forensic research lab. “If you’re Russia and you’re facing increased global scrutiny, increased global closure, you look to countries like India to at least abstain from as many efforts to isolate Russia as humanly possible.”

---------

While India and Russia have long had close ties, researchers say there are signs that social media posts parroting Kremlin talking points may not be legitimate.

In the days after Russia’s invasion of Ukraine, thousands of Twitter accounts shared messages of support for Vladimir V. Putin, the Russian president.

They tried to deflect criticism of the war by comparing it to conflicts instigated by Western countries. Their commentary — along with tweets from other users who condemned it — made the hashtag #IStandWithPutin trend on Twitter in several regions around the world.

While some of the accounts said they were based in Nigeria and South Africa, the majority of those with a declared location on Twitter claimed to be from India and targeted their messages to other Indian users, researchers said.

The prevalence of accounts claiming to be from Indian users indicates that India’s social media landscape has become an important destination in the effort to influence public opinion of the war in Ukraine. Users who said they were from India made up nearly 11 percent of the hashtag trend in the two weeks after the invasion. Just 0.3 percent were from Russia and 1.6 percent from the United States during that time.

---------

The death of an Indian student in the fighting in Ukraine this month brought into focus India’s challenge of evacuating nearly 20,000 of its citizens who were in the country when Russia’s invasion began. Hundreds of Indian students remained stuck amid heavy shelling at the time. India’s prime minister, Narendra Modi, who has avoided condemning Russia, appealed to Mr. Putin and his Ukrainian counterpart, President Volodymyr Zelensky, for help.

Russia’s local embassy used Twitter to instruct Indian media outlets to not use the word “war” but to instead refer to it as a “special military operation,” as media outlets in Russia have been forced by law to do. Some Indian Twitter users responded by mocking the embassy, while others chastised local media outlets as inept and needing instruction from Russia.

Pro-Russian sentiment has taken hold in right-wing circles in the United States, misinformation that has spread within Russia claims Ukrainians have staged bombings or bombed their own neighborhoods, and myths about Ukrainian fortitude have gone viral across social media platforms. But in India and other countries where social media users joined the hashtag, pro-Russian narratives have focused on ethnonationalism and Western hypocrisy over the war, themes that have resonated with social media users.

By VIR SANGHVI

Even while the war in Ukraine rages, however, we should be asking ourselves deeper questions. A few days ago, at the ABP Ideas of India Summit in Mumbai, I interviewed Fareed Zakaria. Fareed’s view was that over the last decade or so, India has become so inward-looking and obsessed with its own issues and divisions that it has not spent enough time thinking about its place in the world, going forward.

While we have been obsessed with headscarves and caste arithmetic, the world has rearranged itself. No matter what happens in Ukraine, Russia will come out of the war damaged. If it makes peace, then some of the sanctions imposed on it by the West may be moderated but it seems unlikely that Putin’s Russia will become a full-fledged member of the global economy for a long time.

In that case, it will have no choice but to move into the Chinese sphere of influence. One scenario sees Russia as a classic vassal state of the Chinese, supplying energy and raw materials to feed the Chinese military machine and its industrial complex. Pakistan and China are longstanding allies, so we will probably see the emergence of a Russia-China-Pakistan alliance.

India will then have two choices. Either we agree to accept China’s suzerainty over the East. Or we look for other options.

Should we choose the second path (and I imagine we will have to), then there really is nowhere to go but the West. At present, the West understands how India is constrained by its dependence on Russian weaponry. But in the long run, it will expect a greater measure of alignment. Is that something we have considered? Or are we too blinded by the rhetoric about anti-Hindu America and hypocritical Washington?

Sooner, rather than later, we will have to rescue reality from the rhetoric.

The Central Government on Thursday more than doubled the price of domestically produced natural gas for the six months beginning tomorrow (1 April), reflecting a surge in global prices.

The Petroleum Planning and Analysis Cell of the federal oil ministry announced the new prices today.

This will raise the prices of gas sold to households, the power sector, industries and fertiliser firms, adding to overall inflation.

As per a notification issued by the oil ministry's PPAC, the price of gas from regulated fields of state-owned Oil and Natural Gas Corp Ltd and Oil India Ltd will rise to a record $6.10 per million British thermal unit from the current $2.90.

The rate paid for difficult fields like deepwater will rise to $9.92 for April-September from $6.13 per mmBtu, the notification stated.

India links prices of locally produced gas from old fields to a formula tied to global benchmarks, including Henry Hub, Alberta gas, NBP and Russian gas.

High natural gas prices will boost earnings of producer ONGC, Oil India Ltd and Reliance Industries.

India's annual retail inflation exceeded 6% for the second consecutive month in February.

Image without a caption

By Fareed Zakaria

https://www.washingtonpost.com/opinions/2022/05/12/biden-sanctions-russia-could-erode-dollar-power-financial-economic/

...the unprecedented nature of these measures (US sanctions against Russia) is producing concerns around the world that the United States has “weaponized” its financial power and could lead, over time, to the decline of the dollar’s dominance, which is what gives America its financial superpowers in the first place.

I’ve been hearing about this firsthand from three sources I trust. The first, in New Delhi, recently told me about a conversation that took place at the highest levels of India’s government. The topic: how to make sure that the United States could never do to India what it has just done to Russia. The second, from Brussels, where staff at the European Commission has been tasked — even while working with Washington on the sanctions — with finding ways to reduce the role of the dollar in its energy imports. The third, an Asian observer of China, speculated that the overly severe lockdowns in Shanghai — which involved the rationing of food and basic supplies — might be part of an effort by Beijing to experiment with a scenario in which it faced economic sanctions from Washington (perhaps after an invasion of Taiwan).

A debate is raging around the world about whether the dollar’s total dominance of the international financial system is waning. Even Goldman Sachs and the IMF have warned that that might well happen. I tend toward the opposite view: Namely, that you can only beat the dollar if you have an effective alternative, which so far does not exist.

But it’s clear that many countries — from hostile powers such as China and Russia to friendly nations such as India and Brazil — are working hard on ways to reduce their vulnerability to Washington’s whims. None of these efforts has so far gained much traction, though it is worth noting that the share of global foreign exchange reserves held in dollars has declined from 72 percent to 59 percent over the past two decades.

Partly this is because the United States appears less stable and predictable in the use of its extraordinary privilege. In the two decades preceding Russia’s invasion, Washington massively ramped up sanctions for all kinds of reasons — by more than 900 percent. Many of these measures were overreactions and should be rolled back. After 9/11, Washington put in place highly intrusive measures aimed at tracking money going to terrorists. It has inflicted harsh punishments on banks that did not adhere to all U.S. sanctions. It has imposed sanctions on Iran, Venezuela, North Korea, Cuba and other countries often simply to satisfy domestic critics who wanted to “do something” without paying much of a price. This type of economic warfare has failed to change the regimes in these countries but has caused widespread misery for ordinary people in them. Sanctions against Russia are aimed at policy change, not regime change, and therefore could be more effective.

----------

The dollar maintains its crucial role in the international system because the United States has the world’s largest economy. It also has the most liquid debt markets, its currency floats freely, and, crucially, it is regarded as a country based on the rule of law and not one prone to arbitrary and unilateral actions. That last criterion is not one that Washington has lived up to in recent years. Biden should make sure that, in fighting this battle against Russia, he does not erode America’s unique financial superpower.

https://twitter.com/haqsmusings/status/1531786077320515585?s=20&t=kz7P7UGmVoe8grxMjJyonA

‘We have a growing suspicion that India is becoming the de facto refining hub for Europe’: RBC’s Tran

In an unexpected twist, the European Union’s plan to ban imports of Russian crude in response to Moscow’s invasion of Ukraine appears to be transforming India’s role in the global oil trade.

“As the EU weans from Russian refined product, we have a growing suspicion that India is becoming the de facto refining hub for Europe,” said Michael Tran, global energy strategist at RBC Capital Markets, in a Tuesday note.

It’s all part of the seismic displacements taking place across the physical market for crude and products in the aftermath of Russia’s late-February invasion and the resulting rounds of sanctions placed on Moscow.

EU leaders agreed Monday to embargo most Russian oil imports into the bloc by year-end as part of new sanctions agreed at a summit. While the agreement marks a hard-fought policy victory for the West, the reshuffling of global trade flows are set to prove economically inflationary for all nations involved as long as the war drags on, Tran said.

That will make sourcing barrels more expensive and keep upward pressure on oil pricing, the analyst said. The U.S. oil benchmark CL.1, 0.44% CLN22, 0.44% ended the day lower on Tuesday after earlier trading near a three-month high just shy of $120, but ended may with a strong gain. Brent crude BRN00, +0.58%, the global benchmark, ended higher and was also up for the month.

Meanwhile, India’s new role comes as it loads up on discounted Russian crude, which it has been refining at a torrid pace and then exporting refined products (see chart below).

Here’s how the puzzle pieces fit together, according to Tran:

India is buying record amounts of severely discounted Russian crude, running its refiners above nameplate capacity, and capturing the economic rent of sky-high crack spreads and exporting gasoline and diesel to Europe. In short, the EU policy of tightening the screws on Russia is a policy win, but the unintended consequence is that Europe is effectively importing inflation to its own citizens. This is not only an economic boon for India, but it also serves as an accelerator for India’s place in the new geopolitically rewritten oil trade map. What we mean is that the EU policy effectively makes India an increasingly vital energy source for Europe. This was historically never the case, and it is why Indian product exports have been clocking in at all-time-high levels over recent months.

So does India’s example mean that Russian crude no longer bound for Europe will just end up elsewhere? That’s unlikely, according to Tran.

He expects the EU ban to back out around 1.2 million to 1.5 million barrels a day (mbd) of Russian exports. They will have to find a home elsewhere, particularly Asia.

So far, China has yet to increase imports, let alone Russian barrels, but scope for India, which has “already been backing up the truck and buying discounted Russian barrels in size,” to further boost purchases appears limited. Over time, Russian storage will fill and production will begin to falter, Tran said.

He noted that Russian floating crude storage now stand near 2 million barrels, down from 3.5 million a month ago, while refined products remain unchanged near 4 million barrels.

“This implies that barrels have continued to move in a relatively fluid state and storage levels have yet to be stressed, for now, but given the ban, the directional arrows of process would suggest that the wheels are in motion,” he said.

Arif Rafiq

@ArifCRafiq

Bangladesh says it seeks to learn from India how it’s managed to import discounted Russia oil without being penalized by the US.

Smaller developing countries envy the exception given to India by the US. They see India as having its cake & eating it too.

https://twitter.com/ArifCRafiq/status/1532083876163624965?s=20&t=trUNGaLYuJ__ZSZWoWXX1g

----------

Momen seeks advice from New Delhi on purchase of Russian oil

India’s oil purchases from Russia have more than doubled from last year, reports BBC

Foreign Minister AK Abdul Momen on Monday said he sought suggestions from India on how they are managing their oil purchases from Russia, noting that the energy issue has become a real problem for Bangladesh too.

“We are dependent on energy (import). Russia offered us energy and wheat. It has become a real problem. We are afraid of the energy crisis. We sought India’s suggestions on how they are doing it. This is more of a friendly discussion,” he told reporters, apparently keeping the fear of sanctions in mind.

Momen attended the two-day NADI Conclave in Guwahati on May 28-29, together with his Indian counterpart S Jaishankar.

According to BBC, the Indian government has defended the move to buy Russian oil, saying what it buys from Russia in a month is less than what Europe buys from Russia in an afternoon.

As calls continue for India to keep its distance from Moscow over the Ukraine issue, its oil purchases from Russia have more than doubled from last year.

India has taken advantage of discounted prices to ramp up oil imports from Russia at a time when global energy prices have been rising.

Without naming any country, Momen said: “You are seeing that they keep bossing us and you (journalists) also encourage them. Every day, they come up with new issues. We used to call them development partners. They do not pay for the development but keep giving advice.”

Momen also claimed that to impede the development, they put forward many things and added various conditions to create instability.

“These are not acceptable,” he added.

Responding to a question, the foreign minister said Bangladesh, being a peace-loving country, always welcomes stability in the world.

“We are very inter-dependent,” he said, adding that Bangladesh will get affected if there is instability in the USA and Europe – two big markets for Bangladesh’s export.

At the same time, if there is instability in the Middle East, Bangladesh’s remittance earnings will get hurt, he said.

“We do not want to get into any problem. We want peace in the world,” Momen said, adding that the rich countries will also be affected and it is good for all to end the war as soon as possible.

https://www.reuters.com/markets/commodities/exclusive-indias-russian-coal-buying-spikes-traders-offer-steep-discounts-2022-06-18/

India's Russian coal buying May 27-June 15 up 6-fold-govt data

India's Russian oil buying May 27-June 15 up 31-fold-govt data

June Russia coal imports seen at multi-year high - Refinitiv

Bulk shipments of Russian thermal coal began third week of May

India's purchases of Russian coal have spiked in recent weeks despite global sanctions on Moscow, as traders offer discounts of up to 30%, according to two trade sources and data reviewed by Reuters.

Russia, facing severe Western sanctions over its invasion of Ukraine, warned the European Union in April against sweeping sanctions on coal, saying they would backfire as the fuel would be redirected to other markets.

India has refrained from condemning Russia, with which it has longstanding political and security ties, while calling for an end to violence in Ukraine. New Delhi defends its purchases of Russian goods as part of an effort to diversify supplies and argues a sudden halt would jack up world prices and hurt its consumers.

U.S. officials have told India there is no ban on energy imports from Russia but they do not want to see a "rapid acceleration".

Yet as European importers shun trade with Moscow, Indian buyers are lapping up huge quantities of Russian coal despite high freight costs.

Its purchases of coal and related products jumped more than six-fold in the 20 days through Wednesday from the same period a year earlier to $331.17 million, according to unpublished Indian government data reviewed by Reuters.

Indian refiners similarly have snapped up cheap Russian oil shunned by Western countries. The value of India's oil trade with Russia in the 20 days through Wednesday jumped more than 31-fold to $2.22 billion, the data showed.

India's trade ministry did not immediately respond to a request for comment on Saturday.

"The Russian traders have been liberal with payment routes and are accepting payments in Indian rupee and United Arab Emirates dirham," one source said. "The discounts are attractive, and this trend of higher Russian coal purchases will continue."

COAL BUYING TO CONTINUE

Offshore units of such Russian coal traders as Suek AG, KTK and Cyprus-based Carbo One in places including Dubai and Singapore offered discounts of 25% to 30%, triggering bulk purchases of Russian thermal coal by traders supplying to utilities and cement makers, the sources said.

The second source said the Singapore-based unit of Suek was also accepting payments in dollars.

Suek and KTK did not immediately respond to requests for comment. Reuters could not immediately reach Carbo One.

The EU ban has barred new coal contracts and by mid-August will force members nations to terminate existing ones.

India bought an average $16.55 million of Russian coal a day in the three weeks through Wednesday, more than double the $7.71 million it bought in the three months after Russia's Feb. 24 invasion, according to Reuters calculations.

Oil purchases averaged $110.86 million a day in the 20-day period, more than triple the $31.16 million it spent in the three months ended May 26.

Indian bulk buying of Russian coal is set to continue, with June imports expected to be the most in at least seven and a half years, Refinitiv Eikon ship tracking data showed.

Bulk shipments of Russian thermal coal started reaching India in the third week of May, with orders mainly from cement and steel firms and traders, according to shipping data compiled by an Indian coal trader.

https://www.wsj.com/articles/us-inflation-june-2022-consumer-price-index-11657664129

U.S. consumer inflation rose to a new four-decade high at an annual rate of 9.1% in June, extending a year and a half stretch of persistently higher prices.

The consumer-price index’s rate of increase last month was the highest since December 1981, the Labor Department said Wednesday. It also eclipsed May’s annual rate of 8.6% that led Federal Reserve officials to shift to a faster pace of benchmark interest-rate increases in its campaign to bring down inflation.

The report likely keeps the Fed on track to raise its benchmark interest rate by 0.75 percentage point at its meeting later this month. Stocks dropped and bond yields jumped following the inflation report.

Core prices, which exclude volatile food and energy components, increased by 5.9% in June from a year earlier, slightly less than May’s 6.0% gain, the Labor Department said.

On a month-to-month basis, core prices rose 0.7% in June, a bit more than their 0.6% increase in May—a sign of inflationary pressures throughout the economy.

The report showed few signs of relief from higher prices. Costs were up broadly across the economy, with gasoline far outpacing other categories with an 11.2% gain over the prior month. Gasoline prices have been on a downward path in recent weeks. Shelter and food price increases were also major contributors to inflation, the Labor Department said.

“This report will make for very uncomfortable reading at the Fed,” said Ian Shepherdson, chief economist at Pantheon Macroeconomics.

Despite June’s inflation reading, economists point to recent developments that could subdue price pressures in the coming months.

Investor expectations of slowing economic growth world-wide have led to a decline in commodity prices in recent weeks, including for oil, copper, wheat and corn, after those prices rose sharply following the Russian invasion of Ukraine. Retailers have warned of the need to discount goods, especially apparel and home goods, that are out of sync with customer preferences as spending shifts to services and away from goods, and consumers spend down elevated savings.

The world, Blair said, was at a turning point in history comparable with the end of World War Two or the collapse of the Soviet Union: but this time the West is clearly not in the ascendant.

"We are coming to the end of Western political and economic dominance," Blair said in a lecture entitled "After Ukraine, What Lessons Now for Western Leadership?" according to a text of the speech to a forum supporting the alliance between the United States and Europe at Ditchley Park west of London.

"The world is going to be at least bi-polar and possibly multi-polar," Blair said. "The biggest geo-political change of this century will come from China not Russia."

Russia's invasion of Ukraine has killed thousands and triggered the most serious crisis in relations between Russia and the West since the 1962 Cuban Missile Crisis, when many people feared the world was on the brink of nuclear war.

President Vladimir Putin says the West has declared economic war by trying to isolate Russia's economy with sanctions and the Kremlin says Russia will turn to powers such as China and India.

The war in Ukraine, Blair said, had clarified that the West could not rely on China "to behave in the way we would consider rational".

Chinese President Xi Jinping has continued supporting Putin and criticised sanctions "abuse" by the West. Putin has forged what he calls a "strategic partnership" with China.

China in 1979 had an economy that was smaller than Italy’s, but after opening to foreign investment and introducing market reforms it has become the world’s second-largest economy.

Its economy is forecast to overtake the United States within a decade and it leads in some 21st century technologies such as artificial intelligence, regenerative medicine and conductive polymers.

"China’s place as a superpower is natural and justified. It is not the Soviet Union," said Blair, who was prime minister from 1997 to 2007. Its allies are likely to be Russia and Iran.

The West should not let China overtake militarily, he said.

"We should increase defence spending and maintain military superiority," Blair said. The United States and its allies "should be superior enough to cater for any eventuality or type of conflict and in all areas."

https://www.reuters.com/business/energy/exclusive-russia-seeking-oil-payments-india-dirhams-sources-document-2022-07-18/

Russia is seeking payment in United Arab Emirates dirhams for oil exports to some Indian customers, three sources said and a document showed, as Moscow moves away from the U.S. dollar to insulate itself from the effects of Western sanctions.

Russia has been hit by a slew of sanctions from the United States and its allies over its invasion of Ukraine in late February, which it terms a "special military operation".

An invoice seen by Reuters shows the bill for supplying oil to one refiner is calculated in dollars while payment is requested in dirhams.

Russian oil major Rosneft is pushing crude through trading firms including Everest Energy and Coral Energy into India, now its second biggest oil buyer after China.

Western sanctions have prompted many oil importers to shun Moscow, pushing spot prices for Russian crude to record discounts against other grades.

That provided Indian refiners, which rarely bought Russian oil due to high freight costs, an opportunity to snap up exports at hefty discounts to Brent and Middle East staples.

Moscow replaced Saudi Arabia as the second biggest oil supplier to India after Iraq for the second month in a row in June.

At least two Indian refiners have already settled some payments in dirhams, the sources said, adding more would make such payments in coming days.

The invoice showed payments to be made to Gazprombank via Mashreq Bank, its correspondent bank in Dubai.

The United Arab Emirates, seeking to maintain what it says is a neutral position, has not imposed sanctions on Moscow, and the payments could add to the frustration of some in the West, who privately say the UAE's position is untenable and siding with Russia..

The trading firms used by Rosneft have started asking for the dollar equivalent payment in dirhams from this month, the sources said.

Rosneft, Coral Energy and Everest Energy did not respond to Reuters emails seeking comment.

Russia wants to increase its use of non-Western currencies for trade with countries such as India, its foreign minister Sergi Lavrov said in April.

The country's finance minister last month also said Moscow may start buying currencies of "friendly" countries, using such holdings to influence the exchange rate of the dollar and euro as a means of countering sharp gains in the rouble.

The Moscow currency exchange is preparing to launch trading in the Uzbek sum and the dirham.

Dubai, the Gulf's financial and business centre, has emerged as a refuge for Russian wealth.

India, also maintaining a neutral position, recongnises insurance cover by Russian companies and has offered classification to ships managed by a Dubai-based subsidiary of Moscow's top shipping group to enable trade.

India's central bank last week introduced a new mechanism for international trade settlements in rupees, which many experts see as a way to promote trade with countries that are under Western sanctions, such as Russia and Iran.

Countries tend to hold certain currencies as reserve assets mostly for economic, not geopolitical, reasons

ISABELLE MATEOS Y LAGO

https://www.ft.com/content/e2a69a2b-8eb1-4164-97ab-7a532cf743a2

"But ultimately, international reserves are held for specific economic reasons, not geopolitical ones: pegging or managing the exchange rate to another currency; paying for imports and international debt service; providing foreign exchange liquidity of last resort to domestic banks. So what will determine the extent of any shift in global reserve allocations is not the portfolio preferences of central bankers or the intrinsic properties of US dollar alternatives. It is whether new currencies come to play an important role in international trade and financial relations. The recent news of China negotiating with Saudi Arabia to pay for oil in renminbi is not, in itself, game-changing. If it finally happens and more of China’s inbound and outbound trade partners follow, it might well be"

-----

Days after Russian troops invaded Ukraine, the G7 and a host of allies in Europe and Asia declared a freeze on the assets of the Central Bank of Russia. The move, unprecedented in its swiftness and scale, instantly incapacitated roughly half of its $630bn in international reserves. Up to this point, central bank reserves had only been frozen multilaterally after abrupt regime change — think of the Bolshevik and Chinese revolutions, or more recently Hugo Chávez’s Venezuela.

Immediately, warnings were uttered about unintended consequences, in particular the stability of the US dollar in the international monetary system. As many have convincingly argued, the Russian reserves freeze alone is unlikely to end the dominant role of the US dollar. But it might, over time, induce major shifts in global monetary relations alongside a broader rewiring of globalisation, making the last 30 years look like a lost golden age.

Prudence and deliberation are in central banks’ DNA. They do not make rash decisions. So while many central bankers privately felt shock or dismay at the reserves freeze, they do not appear to have significantly reallocated assets away from the dollar or euro.

Yet there is consensus among central bank reserve managers that something fundamental has changed: geopolitical considerations now need to be taken into account when assessing the safety and liquidity of a reserve asset. For most, this is an argument in favour of currency diversification, a trend under way already over the past 20 years at the expense of the US dollar and to the benefit of smaller advanced economy currencies such as the Canadian dollar or the Korean won. This might now accelerate, and possibly extend to additional currencies.

Might the renminbi be one of the beneficiaries, as suggested by a recent survey? In fact, when it comes to the attractiveness of Chinese bonds in reserve portfolios after the sanctions on Russia, geopolitics is a clear dividing line. By and large, central bankers I talk to in countries in or close to the sanctioning coalition are reviewing — but not yet retreating from — whatever exposure or planned exposure they had to the renminbi. Others seem more inclined to stick to their holdings and plans to ramp them up further over time.

In the near term there is little practical scope to overhaul trade and financing patterns, even if some countries want to. But other forms of rewiring may develop. Countries that see themselves as politically aligned may try to create a mutual aid system, separate from the sanctioning coalition. China’s recent creation of a renminbi liquidity facility at the Bank for International Settlements can be seen in this light. Discussions could also resurface between large reserve holders from the global south about swap arrangements, like those between the Fed, European Central Bank, Bank of England and a few others in the 2008 financial crisis. Cross-border payment systems to rival Swift will probably continue to grow.

In June, Indian buyers paid for at least 742,000 tonnes of Russian coal using currencies other than the US dollar, according to a summary of deals compiled by a trade source based in India using customs documents and shared with Reuters, equal to 44% of the 1.7 million of tonnes of Russian imports that month.

https://thewire.in/business/indian-companies-are-swapping-dollar-for-asian-currencies-to-buy-russian-coal-data#:~:text=In%20June%2C%20Indian%20buyers%20paid,of%20Russian%20imports%20that%20month.

Indian companies are using Asian currencies more often to pay for Russian coal imports, according to customs documents and industry sources, avoiding the US dollar and cutting the risk of breaching Western sanctions against Moscow.

Reuters previously reported on a large Indian coal deal involving the Chinese yuan, but the customs data underline how non-dollar settlements are becoming commonplace.

India has aggressively stepped up purchases of Russian oil and coal since the war in Ukraine began, helping to cushion Moscow from the effects of sanctions and allowing New Delhi to secure raw materials at discounts compared to supplies from other countries.

Russia became India’s third-largest coal supplier in July, with imports rising by over a fifth compared with June to a record 2.06 million tonnes.

In June, Indian buyers paid for at least 742,000 tonnes of Russian coal using currencies other than the US dollar, according to a summary of deals compiled by a trade source based in India using customs documents and shared with Reuters, equal to 44% of the 1.7 million of tonnes of Russian imports that month.

Indian steelmakers and cement manufacturers have bought Russian coal using the United Arab Emirates dirham, Hong Kong dollar, yuan and euro in recent weeks, according to customs documents separately reviewed by Reuters.

The yuan accounted for 31% of the non-US dollar payments for Russian coal in June and the Hong Kong dollar for 28%. The euro made up under a quarter and the Emirati dirham around one-sixth, the data from the trade source showed.

The Ministry of Finance, which administers the customs board, did not respond to emails seeking comment confirming the documents. The Ministry of Commerce and Industry declined to comment.

The Reserve Bank of India also did not respond to requests for comment.

The RBI has approved payments for commodities in the Indian rupee, a move it expects to boost bilateral trade with Russia in its own currency.

https://www.wsj.com/articles/inflation-jackson-hole-fed-powell-11661288446

Force 1: Globalization. Increased flows of trade, money, people and ideas flourished with the Cold War’s end and China’s entry into the international trading system in the 1990s. Multinational companies using new technologies constructed global supply chains focused on driving down costs by finding the cheapest place and workers to produce products. Worldwide competition drove prices lower for many goods.

This helped keep U.S. inflation stable. Over the 20 years that ended in 2019, U.S. goods prices rose an average of 0.4% a year, while services prices grew 2.6% annually, leaving “core inflation”—which excludes volatile food and energy prices—around 1.7%.

After the pandemic and the Ukraine war disrupted supply chains, many business leaders adopted new processes to increase reliability even if they cost more, such as by moving production closer to home or buying from multiple suppliers. And tensions between Western democracies and Russia and China raise concerns about a possible further retreat from globalization and rise of protectionism, which would raise production costs.

“If you had all of your supply chain in just one country, you have to question why take that risk in a world where pandemics could hit or country relations could deteriorate or wars could happen between countries,” said Richmond Fed President Tom Barkin, a former McKinsey & Co. executive. It is difficult to predict just how durable such changes will be, he added.

Force 2: Labor markets. In an August 2020 book, “The Great Demographic Reversal,” former British central banker Charles Goodhart and economist Manoj Pradhan argued that the low inflation since the 1990s had less to do with central-bank policies and more with the addition of hundreds of millions of low-wage Asian and Eastern European workers, which held down labor costs and prices of manufactured goods exported to richer countries.

Mr. Goodhart wrote that global labor glut was giving way to an era of worker shortages, and hence higher inflation.

Meanwhile, the U.S. labor force has roughly 2.5 million fewer workers since the pandemic began, compared with what it would have if the prepandemic trend in workforce participation had continued and after accounting for the aging of the population, according to an analysis by Didem Tüzemen, an economist at the Kansas City Fed. Its growth had already slowed before Covid-19, reflecting an aging population, declining birthrates and less immigration. The slower growth rate of the U.S. workforce could force wages higher, feeding inflation.

Wages rose about 3% annually before the pandemic. Average hourly earnings grew 5.2% in the year ended in July.

By Abhishek G Bhaya

https://news.cgtn.com/news/2022-09-20/Bangladesh-could-be-a-test-case-for-end-of-dollar-dominance-1dtUjF9qNR6/index.html

Bangladesh is moving to trade in local currencies with two of its largest trading partners – China and India – in a decision that could well prove to be a test case for the end of the U.S. dollar's dominance in global trade.

Last week, Bangladesh allowed its banks to maintain accounts in Chinese yuan for overseas transactions to reduce dependency on the U.S. dollar as the South Asian country grapples to contain its dwindling foreign reserves.

And according to media reports on Monday, India's top lender, State Bank of India, has asked exporters to trade with Bangladesh in rupee and taka warning against settling deals in the U.S. dollar to avoid exposure to Dhaka's falling reserves.

The developments come amid calls from the Shanghai Cooperation Organization (SCO) – which has both China and India as its members – for increasing the use of national currencies for trade among the member countries at its leadership summit in the Uzbek city of Samarkand last week. Bangladesh is not yet an SCO member but has applied for observer status in the Eurasian organization.

The South Asian country's $416-billion economy is facing severe stress due to rapidly increasing food and energy prices with the prolonged Russia-Ukraine conflict further widening its current account deficit. Bangladesh is facing a shortage of foreign currency due to higher import bills and a steep fall in the Bangladeshi taka's value against the U.S. dollar in recent months.

The country's foreign exchange reserves fell from $48 billion last year to $37 billion as of last Friday, which is sufficient for import cover for only five months, according to data from Bangladesh's central bank.

No wonder, Bangladesh wants to lower trade dependency on the U.S. dollar and it does not see a problem in dealing in local currencies, as the country's Commerce Minister Tipu Munshi asserted last week. Responding to a query at an event in Dhaka, Munshi said that Bangladesh's finance ministry is studying the issue and working on ways to implement local currency trade with its key trading partners.

Last week, the Bangladesh central bank allowed local banks to carry out overseas transactions in Chinese yuan. It is important to note that China-Bangladesh bilateral currency cooperation dates back to 2018 when Dhaka had authorized dealers to maintain a foreign currency clearing account with the central bank in the Chinese yuan.

The Bangladesh Bank's latest decision followed demands from major business chambers such as the Metropolitan Chamber of Commerce and Industries (MCCI) of introducing a second currency besides the U.S. dollar for international trading amid the surging taka-dollar exchange rate.

The MCCI proposed the Chinese yuan as Beijing happens to be Dhaka's largest trade partner and also the largest source of imports. The fact that China already has a Cross-Border Inter-Bank Payments System (CIPS) with the Chinese yuan as the trading currency was also a factor in Bangladesh's decision.

If Bangladesh creates a mechanism for bilateral trade in local currency with India – its second largest trade partner – as well, as recent reports indicate, it will go a long way in reducing the country's dependence on the U.S. dollar for international trade.

NAGOYA, Japan -- Toyota Motor said Friday it will exit from automobile production in Russia, citing difficulties supplying key materials and parts in the country amid the war in Ukraine.

The automaker suspended operations at its plant in St. Petersburg on March 4, after the Russian invasion began.

"After six months, we have not been able to resume normal activities and see no indication that we can restart in the future," Japan's top automaker said.

A protracted disruption would hurt Toyota's ability to support its employees, leaving it no choice but to end production in the country, it said. Mounting geopolitical risks in the region are believed to have contributed to the decision as well.

Toyota had continued to pay its factory workers after suspending production, reassigning them to maintenance and other tasks instead. Details regarding the termination process and treatment of employees at the St. Petersburg plant will be ironed out at a later time.

Toyota holds a larger market share in Russia than any other Japanese automaker. It produced 80,000 vehicles and sold 110,000 in the country in 2021.

It began locally producing vehicles in 2007 at St. Petersburg. The plant's lineup included the RAV4 sport utility vehicle and the Camry sedan in 2021.

Nissan Motor, another Japanese automaker, has extended its production freeze at its St. Petersburg plant to the end of December from the end of September.

@SStapczynski

Europe needs "immediate action" to avoid a natural gas shortage in 2023, says the

@IEA

🇪🇺🚨

⚠️ Europe faces a 30bcm shortfall next summer in gas needed to fuel its economy AND sufficiently refill storage

🇷🇺 Next year's challenge: lower Russian supply, higher Chinese LNG demand

https://twitter.com/SStapczynski/status/1588144104268959744?s=20&t=IrMYdEfyiZifqCO3PD8Aqw

https://www.intellinews.com/russia-s-international-reserves-up-3-6bn-in-one-week-to-571bn-253235/